TSP Loan vs Allotment Loan: Which One Actually Fits Your Emergency

Last updated: June 2026

A TSP loan pulls money out of your own retirement account.

An allotment loan is a separate installment loan, repaid through payroll deduction, that leaves your TSP alone.

Both can cover an emergency.

They put the risk in two completely different places, and that’s the only decision that actually matters here.

If you’re a federal or USPS employee staring down a bill you didn’t see coming, this is the plain-English version of how each one works, where each one can hurt you, and how to pick without guessing.

Who This Is For

- You’re a civilian federal or USPS employee with an emergency bill: car repair, rent, medical, utilities.

- You have a TSP balance, but you’re not sure if touching it is smart.

- You’ve heard of allotment loans and want a straight comparison, not a sales pitch.

You don’t need a finance degree. You need to know which option costs you less in the long run.

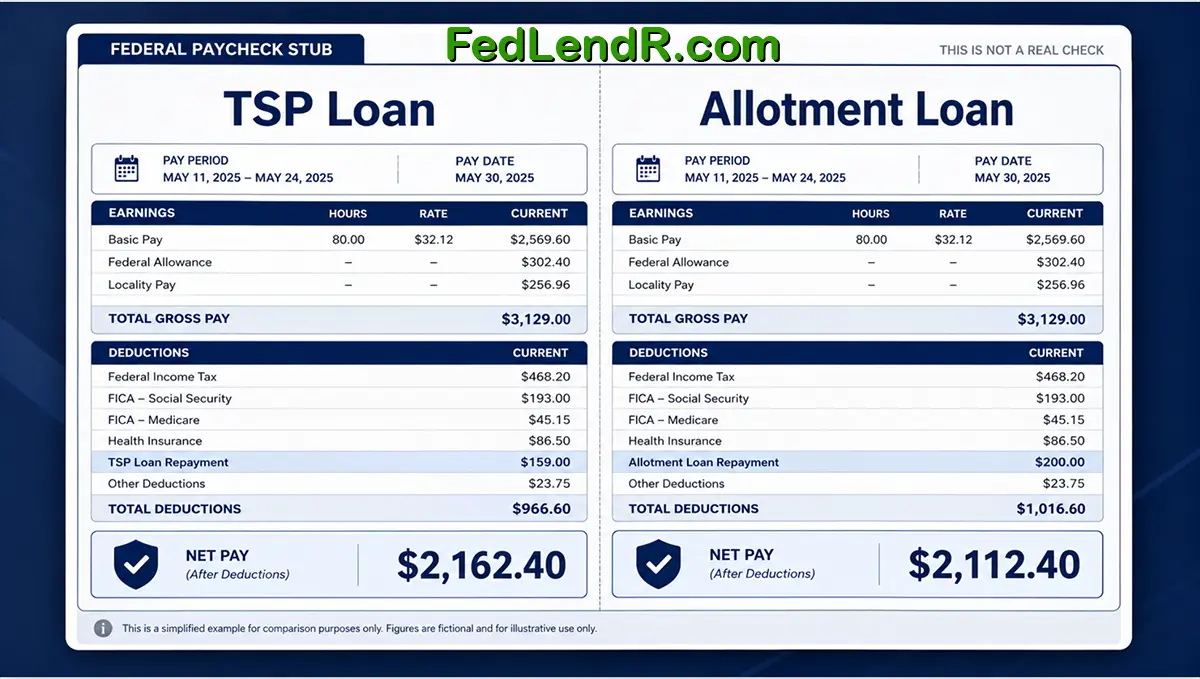

What Is a TSP Loan

A TSP loan is money you borrow from your own Thrift Savings Plan balance.

You’re not borrowing from a bank.

You’re pulling from your own retirement account and paying it back, with interest, through payroll deduction.

The mechanics:

- You need an active TSP balance and federal or USPS employment.

- You can typically borrow a portion of your vested balance, up to set limits.

- Repayment comes out of your paycheck automatically.

- The interest you pay goes back into your own TSP account, not to a bank.

- If you leave federal service with the loan unpaid, the remaining balance can be treated as a taxable distribution. That means taxes, and possibly penalties.

Here’s the part most people skip: while that money is out of your account, it isn’t invested.

If the market moves while your balance is sitting on the sidelines, you don’t get that growth back.

And if you cut your contributions to afford the loan payment, you can lose your agency match too.

That’s not “borrowing from yourself” for free. That’s a real cost, just one that doesn’t show up on a bill.

What Is an Allotment Loan

An allotment loan is a personal installment loan from an independent lender, repaid through a scheduled payroll deduction.

Your TSP never enters the picture.

- You apply through a lending partner that works with federal and USPS employees.

- If approved, you get a lump sum for the emergency.

- Payments come out of your paycheck as an allotment, not a bank draft.

- Your TSP balance and retirement timeline stay untouched.

- Cost, terms, and amount depend entirely on the lender and your state.

Check what you might qualify for — it takes about three minutes, and your federal or USPS employment is the qualification that matters most, not a perfect credit score.

FedLendR.com connects federal and USPS workers with independent lending partners who may offer this kind of payroll-deduction loan.

We’re not a lender.

We can’t guarantee approval or a specific amount.

Every application gets reviewed on its own.

TSP Loan vs Allotment Loan vs Standard Personal Loan

| Feature | TSP Loan | Allotment Loan | Standard Personal Loan |

|---|---|---|---|

| Source of funds | Your own TSP balance | Independent lender | Bank, credit union, or online lender |

| Touches your retirement | Yes | No Better | No Better |

| How it's repaid | Payroll deduction, back into TSP | Payroll allotment | Bank draft |

| If you leave service | Unpaid balance may be taxable | You still owe it, payment method may change | You still owe it |

| Review process | TSP rules, no credit check | Lender review, varies | Lender review, varies |

| Best fit | Larger, planned expenses | Small to mid-size emergencies | Wide range of needs |

When a TSP Loan Makes More Sense

- The expense is large and planned. A priced-out home repair or medical procedure, not a surprise.

- Your job is stable. You’re not eyeing the exit anytime soon, so the separation-tax risk is low.

- You’re chasing the lowest total cost. Since the interest goes back into your account, the effective cost can be lower than other options.

- You’ll keep contributing. You’re disciplined enough to maintain at least the match-eligible contribution while repaying.

Before you pull the trigger, answer these:

- How does this change your retirement timeline?

- What happens if your paycheck shrinks or other bills climb?

- What’s your plan if you change jobs sooner than expected?

Talk to a TSP representative or a benefits counselor before you borrow from your own retirement.

This is education, not personal financial advice.

When an Allotment Loan Makes More Sense

- The emergency is real but the number is moderate. A $900 repair, a late utility bill, a school expense.

- You want your TSP untouched. Especially if you’re close to retirement or already behind on your balance.

- You want one predictable payment. Payroll deduction means you’re not relying on yourself to remember a due date.

- You’d rather keep retirement and short-term borrowing in separate lanes. No paperwork inside your TSP account.

See allotment-friendly loan options that may fit your paycheck

Tradeoffs still apply here: costs and terms vary by lender and state, and overborrowing is overborrowing, even with a tidy payroll deduction attached.

Real Example: The $2,000 Car Repair

Chris is a GS-7 at the IRS. The car needs a $2,000 repair or there’s no way to get to work.

Option 1, TSP loan: Chris has a solid balance. A TSP loan covers the full $2,000, repaid through payroll deduction. Chris understands that $2,000 won’t be invested for a while.

Option 2, allotment loan: Chris checks allotment options through a lending partner, borrows $1,400 instead because the shop will arrange a short payment plan for the rest, and keeps the payroll deduction payment small enough to not strain the budget.

The lesson isn’t which option wins. It’s that Chris borrowed only what was needed and matched the payment to the real paycheck, not the max available.

Real Example: The USPS Carrier Two Years From Retirement

Maria is a USPS carrier with 25-plus years in. A family medical issue creates an $1,100 gap. She’s two to three years from retirement and doesn’t want to touch her TSP this late, especially with separation risk in play if she leaves earlier than planned.

She goes with a short-term allotment loan instead, timed to pay off before retirement, and leaves the TSP alone.

This doesn’t mean everyone near retirement should avoid a TSP loan. It means the calculation changes when the finish line is close.

How To Decide: 6 Steps

- Write down the real number. Strip out anything that isn’t the actual emergency cost.

- Check your budget, not your pay stub. Look at the last two or three months of real spending before you commit to a payment.

- Check your TSP timeline. Years to retirement, comfort with a smaller balance if the market dips, and whether you’ll keep enough contribution to hit your match.

- Understand the exit risk. A TSP loan turns into a tax bill if you leave service unpaid. An allotment loan just follows you, and the lender may switch your payment method.

- Read the fine print. Pull the official TSP loan booklet for a TSP loan. Pull the lender’s disclosures for an allotment loan. FedLendR is not a lender, and no partner guarantees approval.

- Get a second opinion if you’re unsure. A financial counselor, your agency’s employee assistance program, or a TSP representative can all weigh in for free.

What we do:

- Run a secure, confidential online form

- Share your information with independent lending partners who may offer payroll allotment loans to federal and USPS employees

- Let you compare what’s available in one place

What we don’t do:

- We are not a lender

- We don’t make credit decisions

- We don’t guarantee approval, amount, timing, or terms

- We don’t serve active duty military

Myths That Cost People Money

“A TSP loan is free since I’m paying myself back.” The interest goes back into your account, but the money is out of the market while the loan is outstanding. Cut contributions to cover the payment, and your final balance can end up lower than if you’d never borrowed.

“An allotment loan is easy money, so take the max.” Every dollar borrowed is a dollar repaid with cost attached. Borrow the number from Step 1, not the number you’re approved for.

“If I leave my job with a TSP loan, it just follows me quietly.” It doesn’t. An unpaid balance can become a taxable distribution the day you separate.

“Once I’m behind, more debt is the only answer.” Sometimes a loan bridges the gap. Sometimes a call to your creditors or a session with a counselor does more good than another payment on your plate.

Quick-Start Checklist

- Write the exact emergency number

- Set the max payment your real budget can absorb

- Check your TSP balance, timeline, and risk tolerance

- List the pros and cons of a TSP loan for your situation

- List the pros and cons of an allotment loan for your situation

- Factor in a possible job change in the next few years

- Talk to a professional if you’re still on the fence

- Borrow the smallest amount that solves the problem

Bottom Line

Both options answer the same question: how do you cover today without wrecking tomorrow.

Neither one is automatically right.

The TSP loan risks your retirement growth and a tax bill if you leave service early.

The allotment loan risks a new monthly payment you have to manage like any other bill.

Pick based on your timeline, your job stability, and the smallest number that actually solves the problem in front of you.

Frequently Asked Questions

1. What’s the main difference between a TSP loan and an allotment loan? A TSP loan uses your own retirement money and directly affects your TSP balance. An allotment loan is a separate installment loan from an independent lender, repaid through payroll deduction, that never touches your TSP.

2. Is a TSP loan always cheaper than an allotment loan? Not always. The TSP loan’s interest goes back into your own account, which can lower its effective cost, but it also pulls money out of the market while it’s outstanding. An allotment loan may cost more on paper but leaves your retirement intact. The real cost depends on the lender’s terms and how long you carry either loan.

3. Which is safer, a TSP loan or an allotment loan? Neither is automatically safer. A TSP loan can feel safer with stable employment and a clear repayment plan. An allotment loan can feel safer if protecting your retirement balance matters more right now. Both carry risk if you overborrow or your job situation changes. Talk to a financial professional before deciding.

4. What happens to my TSP loan if I leave federal service? An unpaid balance can be treated as a taxable distribution, which means income taxes and possibly an early withdrawal penalty. Rules around repayment and rollover exist but can change, so check current TSP guidance or talk to a tax professional before you separate.

5. Do allotment loans require perfect credit? No. Lending partners set their own criteria, and some work with applicants who don’t have perfect credit. Approval is never guaranteed, and terms vary by lender and state. Every application gets reviewed individually.

6. Can I use a TSP loan instead of a short-term, high-cost loan? Some federal employees do, but a TSP loan still carries real risk to retirement growth and a possible tax bill if you separate before it’s repaid. It’s not automatically the better choice just because it’s tied to your own account. Compare the actual terms before deciding.

7. How fast can I get funded through an allotment loan? If approved, funds may be available as soon as the next business day. Timing depends on the lender and your bank’s processing schedule. Speed and approval are never guaranteed.

8. Is FedLendR a federal government loan program? No. FedLendR.com is a private website, not affiliated with the federal government. We connect federal and USPS employees with independent lending partners. Any loan agreement is between you and that lender, not FedLendR or your agency.

9. Are these loans available to active duty military? No. FedLendR does not serve active duty military. Service members have separate protections under federal law and should use resources built specifically for them.

10. Is this article personal financial advice? No. This is general education only, not tax, legal, investment, or personalized financial advice. Talk to a financial planner, benefits counselor, or TSP representative before borrowing against your retirement or taking on a new loan.

Allotment Loans for Federal Employees and USPS Workers

The full overview of how allotment loans work and who qualifies.

Allotment Loans for Postal Employees

USPS-specific details on payroll deduction loans and LiteBlue setup.

Allotment Loans Guide

A step-by-step walkthrough of the application and funding process.

FedLendR Blog

More guides on emergency funding options for federal and USPS workers.

Written by Jer Ayles | 20+ years in consumer lending | About FedLendR